Save

Save Print

Print

The 22nd China Ferro-alloys International Conference, host ed by Ferro-Alloys.com, will be held on 20 May to 22 May, 2026 in Beijing city, China. We sincerely invite you jointly explore the development ferroalloys trend in 2026. Why Attend?

[Ferro-Alloys.com] Eramet: Strong Turnover Momentum in Q1 2026 Driven by A Solid Operational Performance

Christel Bories, Eramet group Chair and CEO:

This first quarter confirmed the Group’s ability to adapt and mobilise to meet its targets, despite the uncertainties.

Our turnover significantly increased, driven by the ramp-up in our Lithium activity in Argentina and the rise in volumes of transported manganese ore in Gabon. The favourable price momentum was largely offset by the fall in the US dollar and rising input costs.

Thanks to our robust technology and a successful ramp-up, our world-class lithium asset in Argentina, started to contribute to our results. In Senegal, in two months, our teams succeeded in managing the effects of the fire that broke out at our mineral sands extraction unit and in providing a technical solution enabling the start of a gradual and partial restart of installations from end-April.

Parallel to this, with the support of our reference shareholders, we made progress in executing our funding plan, notably by submitting the necessary resolutions for a vote on a capital increase at our next General Meeting. We are also working closely with the Board of Directors to appoint a new Chief Executive Officer as soon as possible.

In a disrupted macroeconomic environment, our teams are fully mobilised and focused on our priorities: safety, operational performance and cash management. I am confident in the momentum we have gained and our ability to overcome our challenges by leveraging our exceptional mining assets.

2026 Targets:Transported manganese ore: confirmed between 6.4 and 6.8 Mt with a FOB cash cost3 still between $2.4 and $2.6/dmtu4

- Eramet group adjusted turnover by activity

|

Millions of euros |

Q1 |

Q1 |

Chg. |

Chg. |

|

Manganese |

464 |

457 |

+7 |

+2% |

|

Manganese ore activity |

271 |

250 |

+21 |

+8% |

|

Manganese alloys activity |

193 |

207 |

-15 |

-7% |

|

Adjusted Nickel (excluding SLN) |

163 |

114 |

+49 |

+43% |

|

Share of PT WBN (38.7% - excluding off-take contract) |

116 |

73 |

+43 |

+59% |

|

Weda Bay (trading activity, off-take contract) |

47 |

41 |

+6 |

+15% |

|

Mineral Sands |

39 |

68 |

-29 |

-42% |

|

Lithium |

57 |

0 |

+57 |

n.a. |

|

Holding and eliminations |

117 |

104 |

+13 |

+12% |

|

Eramet group adjusted |

840 |

742 |

+98 |

+13% |

Manganese

In Q1 2026, the solid mining and rail performance in Gabon enabled the transportation of 1.6 Mt of manganese ore (+16% vs. Q1 2025).

Turnover of the Manganese activities was €464m (+2%) for the period:

- Ore: turnover up 8%, driven by rising volumes sold externally and a higher average selling price (+8%), notably driven by the increase in sea freight, but offset by an unfavourable currency effect (-11%);

- Alloys: turnover down 7%, penalised by an unfavourable mix and currency effect, which was partly offset by the increase in volume sold.

|

Manganese ore |

Q1 2026 |

Q1 2025 |

Chg. |

Chg.(%) |

|

Turnover – €m |

271 |

250 |

+21 |

+8% |

|

Manganese ore and sinter transportation – Mt |

1.6 |

1.4 |

+0.2 |

+16% |

|

External manganese ore sales – Mt |

1.4 |

1.2 |

+0.1 |

+10% |

|

FOB cash cost2 (excl. export duties) – $/dmtu |

2.5 |

2.4 |

+0.1 |

+5% |

|

Manganese alloys |

Q1 2026 |

Q1 2025 |

Chg. |

Chg.(%) |

|

Turnover – €m |

193 |

207 |

-15 |

-7% |

|

Alloys sales – kt |

158 |

149 |

+9 |

+6% |

|

o/w refined alloys (%) |

49% |

53% |

-4 pts |

-8% |

Market trends & prices

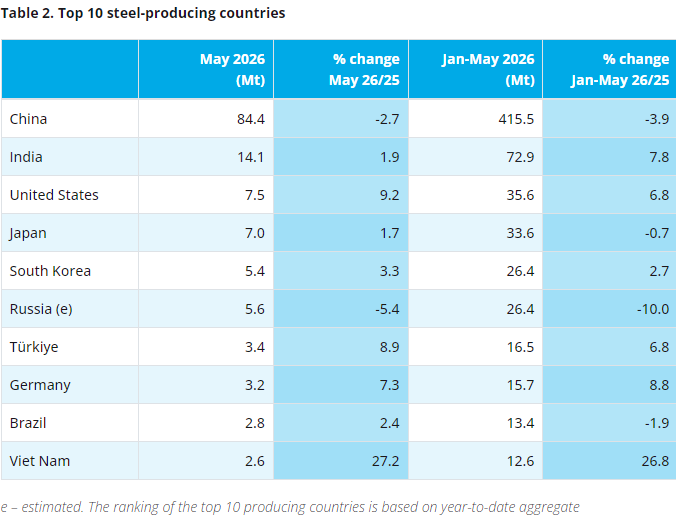

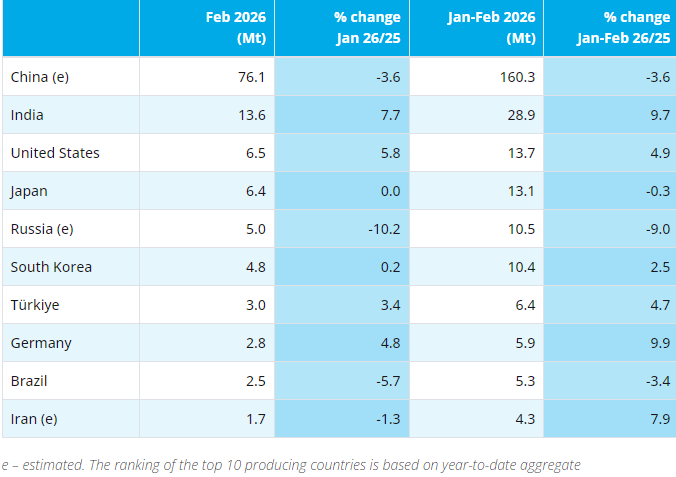

Global production of carbon steel, the main end-product for manganese, was 473 Mt in Q1 2026, down by 2% from Q1 2025.

China, which accounts for more than half of global steel production, was down by nearly 4%. Conversely, India continued to see an increase in production (+9%), which was also the case in North America (+3%), benefitting from the protectionist measures introduced. Europe posted a further decline of 3%, faced with continued declining demand and continuing pressure from imports.

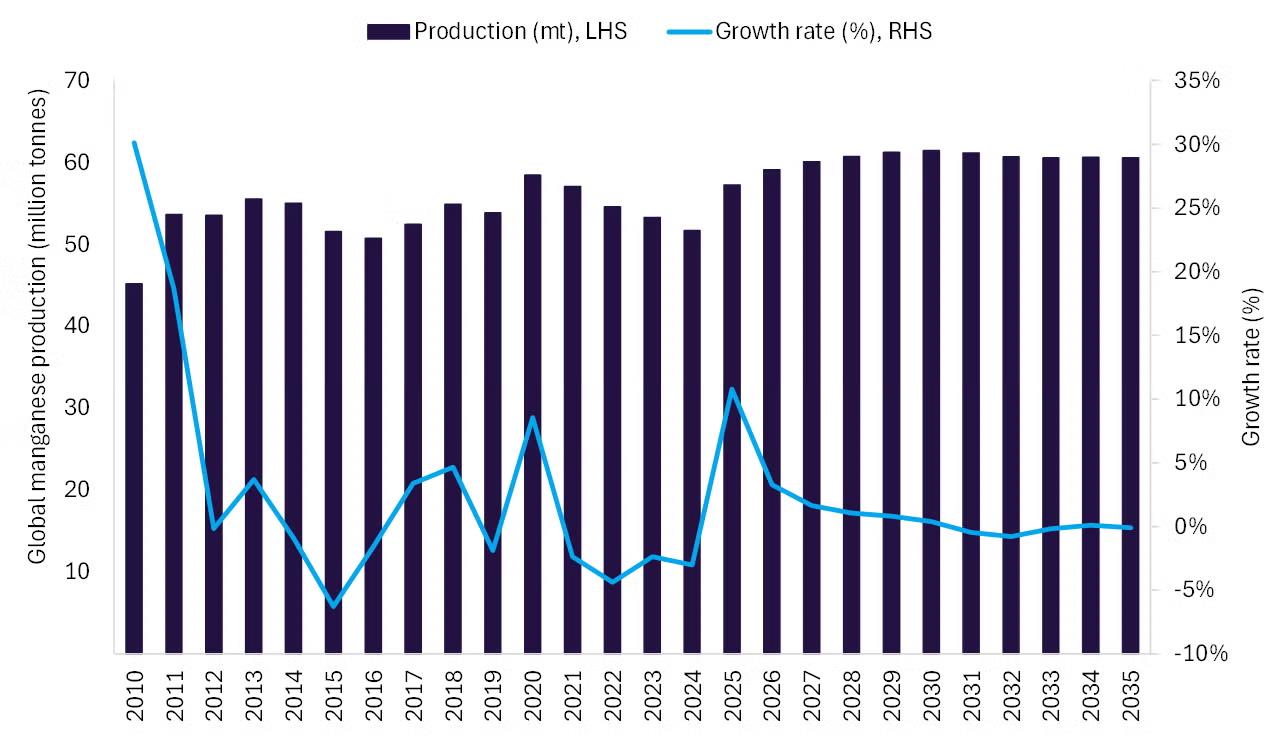

Manganese ore consumption for Q1 2026 reached 5.1 Mt-Mn, up 2% year-on-year, reflecting rising demand from India. In parallel, manganese ore production increased by 13% to 5.3 Mt-Mn, with limited growth for high-grade ore. Production from South Africa, which still accounts for nearly 50% of seaborne production, continued to post record levels (+22%). Gabon also saw volumes up by 4%, in line with the increase in shipments from Comilog over the quarter.

As a result, the manganese ore supply/demand balance was in surplus in Q1 2026, with a more balanced scenario for high-grade (vs. semi-carbonated) ore. Chinese port ore inventories rose to 5.2 Mt at end-March (vs. 4.6 Mt at end-December 2025), representing the equivalent of around 10 weeks of consumption.

The price index for manganese ore (CIF China 44%) averaged $5.0/dmtu in Q1 2026, up 8% vs. Q1 2025 (+11% vs. Q4 2025), boosted by demand that remained strong among manganese alloys producers and mounting pressure on freight costs since early 2026.

The price index for refined alloys in Europe (MC Ferromanganese) averaged €1,523/t, up 2% (+14% vs. Q4 2025), driven by a temporary rise in prices following the introduction of the CBAM (“Carbon Border Adjustment Mechanism”) in Europe. The price index for standard alloys (Silicomanganese) averaged €1,126/t, up 4% (+11% vs. Q4 2025), bolstered by the formal adoption of safeguard measures by the European Union (“EU”). However, US prices are an exception, continuing to face competitive pressure from Indian imports, affecting both standard and refined alloys.

Activities

In Gabon, mining and rail activities delivered a solid performance in Q1 2026, compared to a Q1 2025 disrupted by logistics challenges at the port of Owendo.

The strong operational performance of Setrag enabled the transportation of 1.6 Mt of ore over the quarter (+16% vs. Q1 2025). This momentum, observed both for Comilog flows and for other railway users, reflects tangible progress in terms of safety, traffic and maintenance. Works to modernise the Transgabonese railway are also actively ongoing.

Production is aligned at 1.6 Mt (-11% vs. Q1 2025). Volumes sold externally totalled 1.4 Mt over the quarter (+10% vs. Q1 2025).

The FOB cash cost3 for manganese ore activity averaged $2.5/dmtu over the quarter, up 5% from Q1 2025, reflecting an unfavourable currency effect, which was partly offset by rising volumes. Mining taxes and royalties came out to $0.2/dmtu, stable from Q1 2025. Sea transport costs per tonne were significantly up to $0.9/dmtu (+15%), reflecting the recent increase in freight and fuel rates in connection with the geopolitical situation in the Middle East.

Manganese alloys production slightly increased to 168 kt (4%). Parallel to this, manganese alloys sales were up 6% to 158 kt, with an unfavourable mix notably reflecting the increased volumes of commodities sold in the United States and the rest of the world.

Outlook

Global carbon steel production is expected to moderately increase in 2026, with a less significant decline in Chinese production than in 2025, offset by an increase for the rest of the world – particularly in India where Eramet has a strong business footprint.

As a result, demand for manganese ore should slightly increase in 2026, driven by growth in alloys production in India and the rest of the world, while demand in China is set to remain under pressure. Subject to fuel availability, supply is also expected to remain higher in 2026 than in 2025, driven by continued strong production in South Africa and normalised production levels in Australia.

The market consensus is still set around $5.0/dmtu14 on average for 2026, representing an increase of close to 10% in the manganese ore price index (CIF China 44%) compared with 2025.

As disclosed at the end of February, transported ore volumes are set to be between 6.4 Mt and 6.8 Mt in 2026. The FOB cash cost3 is still expected to be between $2.4 and $2.6/dmtu, with the favourable impact of increased volumes versus 2025 largely offset by an unfavourable currency effect15.

Manganese alloys sales are expected to increase over the year. The activity’s cost base should be impacted from end-Q2 by the recent rise in manganese ore and freight prices – in connection with geopolitical tensions in the Middle East. These cost increases were reflected in the manganese alloys margin with a lag of around 3 months, factoring in the management of inventories and supplies.

- Outlook

The outbreak of the Middle Eastern conflict in late February 2026 was the main unforeseen shock at the start of the year, disrupting trade flows through the Strait of Hormuz. The effects of this conflict on global value chains are not yet fully visible, meaning that the macroeconomic impacts could take time to materialise, with a lag, and highly mixed regional performances. The International Monetary Fund (“IMF”) initiated a downgrade its global growth forecast to 3.1% for 2026 (from 3.3% previously), warning of the risk of a sustained resurgence in inflation.

The average price consensus and exchange rate for 2026 currently stand at:

- around $5.0/dmtu for manganese ore (CIF China 44%),

- c.$16,700/t for LME nickel,

- c.$18,550/t-LCE for lithium carbonate (battery-grade, CIF Asia),

- 1.19 for the $/€ exchange rate.

As a reminder, in early January, the Group had exceptionally set up a hedge on its EUR/USD exposure. The latter concerns around half of its annual exposure33 at end-March with a rate of 1.20.

Manganese alloys selling prices are still expected to face high volatility in 2026.

Market prices for nickel ore in Indonesia should continue to trend positively, supported by both high nickel prices and high premiums on the HPM, in a context of persistent tension on domestic ore supply.

Sensitivities of adjusted EBITDA to the price of metals, to the fuel and to the exchange rate are presented in Appendix .

In 2026, sea freight rates are expected to be at levels higher than in 2025, with increased volatility.

Energy costs are expected to rise, particularly for fuel oil, driven by geopolitical tensions, although alloy production sites – which are highly electricity-intensive – benefit from electricity cost hedging. The cost of reductants is expected to increase slightly over the year.

- Guidance 2026 targets

|

Activities |

Indicators |

18/02/2026 |

23/04/2026 |

|

Manganese |

Transported volumes |

6.4 - 6.8 Mt |

Confirmed |

|

FOB cash cost |

$2.4 - $2.6/dmtu |

Confirmed |

|

|

Alloys sales |

Stable vs. 2025 |

Confirmed |

Quarterly turnover

|

Millions of euros |

Q1 2026 |

Q4 2025 |

Q3 2025 |

Q2 2025 |

Q1 2025 |

|

Manganese |

464 |

474 |

421 |

492 |

457 |

|

Manganese ore activity |

271 |

264 |

221 |

275 |

250 |

|

Manganese alloys activity |

193 |

210 |

200 |

217 |

207 |

|

Adjusted Nickel |

163 |

245 |

142 |

117 |

114 |

|

Mineral Sands |

39 |

55 |

51 |

67 |

68 |

|

Lithium |

57 |

30 |

7 |

4 |

0 |

|

Holding, elim. and others |

117 |

105 |

98 |

105 |

104 |

|

Eramet group adjusted |

840 |

907 |

720 |

786 |

742 |

|

SLN turnover4 |

8 |

7 |

9 |

13 |

19 |

|

Eramet group published financial statements |

732 |

708 |

641 |

716 |

688 |

Productions and shipments

|

Q1 |

Q4 |

Q3 |

Q2 |

Q1 |

Chg. Q1 2026 – Q1 2025 |

|

|

Manganese |

||||||

|

Manganese ore and sinter production (Mt) |

1,595 |

1,680 |

1,874 |

1,764 |

1,785 |

-11% |

|

Manganese ore and sinter transportation (Mt) |

1,608 |

1,517 |

1,586 |

1,659 |

1,386 |

+16% |

|

External manganese ore sales (Mt) |

1,359 |

1,572 |

1,245 |

1,432 |

1,240 |

+10% |

|

Manganese alloys production (kt) |

168 |

157 |

174 |

160 |

162 |

+4% |

|

Manganese alloys sales (kt) |

158 |

174 |

156 |

161 |

149 |

+6% |

Price and index

|

Q1 |

Q4 |

Q1 |

Chg. Q1 2026 – Q1 2025 |

Chg. Q1 2026 – Q4 2025 |

|

|

Manganese |

|||||

|

Mn CIF China 44% ($/dmtu) |

5.02 |

4.53 |

4.64 |

+8% |

+11% |

|

Ferromanganese MC – Europe (€/t) |

1,523 |

1,330 |

1,487 |

+2% |

+14% |

|

Silicomanganese – Europe (€/t) |

1,126 |

1,014 |

1,087 |

+4% |

+11% |

- [Editor:tianyawei]

Daily News

Daily News Research

Research Magazine

Magazine Company Database

Company Database Customized Database

Customized Database Conferences

Conferences Advertisement

Advertisement Trade

Trade

.jpg)

Online inquiry

Online inquiry Contact

Contact

Tell Us What You Think